Clients Paying Late? How Invoice Financing UK Helps Businesses Stay Cash Flow Positive

You’ve smashed a project, the client is thrilled, and the invoice has been sent. Now, you wait. And wait. In a perfect world, that “30-day” term would be a hard deadline, but in the real world, “Net 30” often turns into “Net 45” or even “Net 60.”

For a scaling business in the UK, those missing thousands aren’t just numbers on a screen—they are your next payroll, your stock order, or the marketing budget for your next big push. Late payments are more than a nuisance; they are a literal roadblock to momentum.

This is where invoice financing UK comes into play. It’s one of those financial tools that sounds complex but is actually one of the most straightforward ways to bridge the gap between “job done” and “getting paid.”

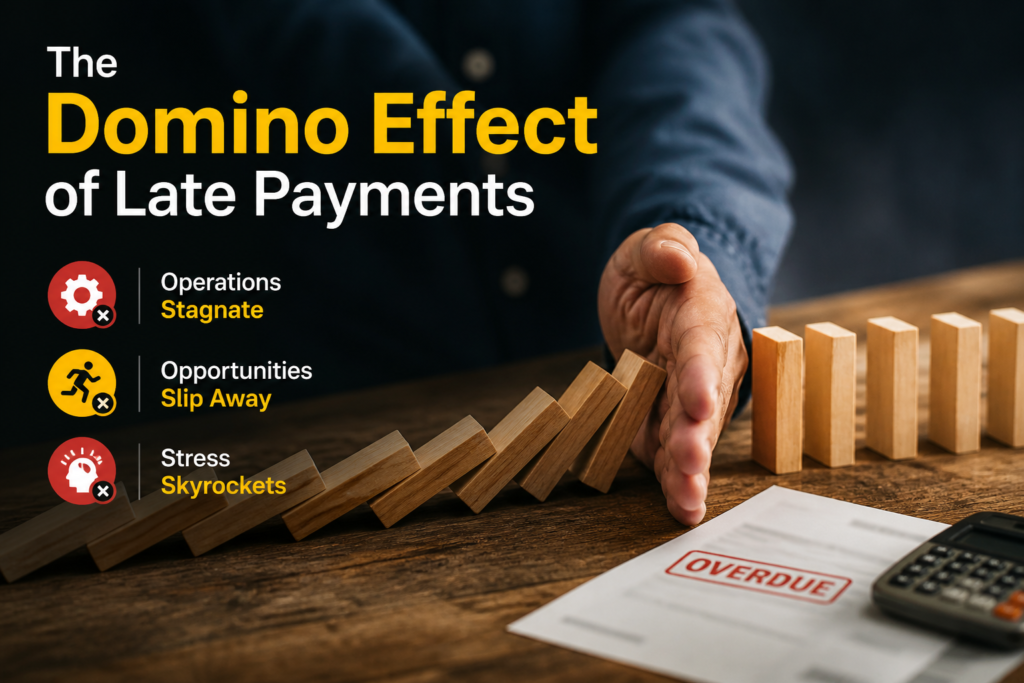

The Domino Effect of Late Payments

In the UK, the culture of late payments is a well-documented struggle. Large corporations often use smaller suppliers as interest-free overdrafts, holding onto cash to pad their own balances while the “little guy” scrambles. When your cash is locked in an unpaid invoice:

- Operations Stagnate: You can’t hire the extra pair of hands you need.

- Opportunities Slip Away: You might have to turn down a big new contract because you can’t afford the upfront materials.

- Stress Skyrockets: Managing a business is hard enough without checking your bank balance every hour to see if “Company X” has finally hit ‘send’ on that transfer.

What Exactly is Invoice Financing?

Think of invoice financing UK as a way to unlock the money you’ve already earned. Instead of waiting weeks for a client to pay, a finance provider “buys” the invoice from you.

They typically advance you about 80% to 90% of the invoice value within 24 hours. Once your client eventually pays the bill, the provider sends you the remaining balance, minus a small fee for their service. It’s your money, just faster.

Two Main Types of Invoice Financing UK: Factoring vs Discounting in 2026

When you start looking at invoice finance providers, you’ll generally see two main paths:

- Invoice Factoring:– This is great if you want to outsource the headache. The provider manages your sales ledger and handles the credit control (the chasing of payments). It’s a huge time-saver, though your clients will know you’re using a finance service.

- Invoice Discounting:– This is the “stealth” version. You keep control of your own collections and chase your own clients. They never need to know you’ve drawn the funds early. More established businesses prefer this with their own accounts teams.

Why It’s a Game Changer for Cash Flow

The beauty of this setup is that it grows with you. Unlike a traditional bank loan with a fixed limit, invoice finance is scalable. The more you invoice, the more funding becomes available. It’s a flexible safety net that ensures you are always “cash flow positive.”

Instead of being at the mercy of your slowest-paying client, you regain control. You can pay your suppliers early (sometimes even snagging an early-settlement discount!), stay on top of VAT bills, and—most importantly—breathe a little easier.

Choosing Between Finance Providers

Not all providers are created equal. The UK market is bustling with options, from high-street banks to fintech startups. When hunting for the right partner, keep these three things in mind:

- The “All-In” Cost:– Look past the initial interest rate. Check for service fees, setup costs, or “drawdown” charges.

- The Human Factor:– If things get tricky, do you want an automated dashboard or a dedicated account manager you can call?

- Flexibility:– Some providers lock you into a 12-month contract for your whole turnover. Others allow “selective” invoice finance, where you only fund specific invoices when you need a boost.

Best Invoice Finance: Your Invoice Financing UK Solution

When it comes to the heavy hitters in the UK market, Best Invoice Finance offers a distinct advantage for businesses that don’t fit the “cookie-cutter” mould of high-street banks.

While many providers focus purely on the numbers, Best Invoice Finance tends to specialise in high-touch, tailored facilities. Here’s how we can specifically help your business overcome the late-payment hurdle:

- Protection Against Bad Debt:- We offer Non-Recourse Factoring, which essentially acts as an insurance policy. If your customer becomes insolvent and can’t pay the invoice, we absorb the loss.

- Sector-Specific Expertise:– Best Invoice Finance is well-regarded for supporting sectors with complex billing cycles—such as construction, recruitment, and manufacturing.

- High Advance Rates:- While some lenders might play it safe with a 70% advance, Best Invoice Finance frequently offers up to 90% of the invoice value upfront.

If you value a partner who looks at the “story” behind your business rather than just a credit score, Best Invoice Finance is a strong contender. We are particularly effective for UK SMEs that need more than just a digital dashboard.

Also Read:- How to Choose the Best Invoice Finance for Startups and Small Businesses

Final Thoughts: Stop Playing the Waiting Game

Late payments shouldn’t be the reason your business fails to reach its potential. By leveraging invoice financing UK, you turn your accounts receivable into a liquid asset. It’s about moving away from “I hope they pay soon” to “I have the capital to grow today.”

If you’re tired of the “cheque is in the post” excuse, it might be time to see what your unpaid invoices could do for you right now.

FAQs

Q. Is invoice financing a loan?

Ans:- Not exactly. It’s a money advance you’ve already earned. You aren’t taking on “new” debt in the traditional sense; you’re just getting access to your own capital earlier.

Q. Will my clients know I’m using it?

Ans:- Only if you choose Invoice Factoring, or if you opt for Invoice Discounting, the arrangement remains confidential, and you continue to handle all client communication.

Q. What happens if a client never pays?

Ans:- It depends on whether you have “Recourse” or “Non-Recourse” finance. With Recourse, you are responsible if the client defaults. Non-Recourse includes insurance to protect you against bad debt.

Q. Is it expensive?

Ans:- Fees vary among invoice finance providers, but for many, the cost is offset by the ability to take on more work or negotiate better rates with their own suppliers.

Q. How fast can I get the money?

Ans:- Once the facility is set up, most providers can deposit funds into your account within 24 hours of you uploading a valid invoice.

Discover the Latest Trends

Stay informed with our latest articles and resources.