Best Invoice Finance Options UK: Factoring vs Discounting vs Spot Finance Explained

Waiting 30, 60, or even 90 days for clients to settle their bills is one of the most frustrating parts of running a business. You’ve successfully completed the work, wrapped up the project, and sent over a beautifully formatted invoice.

Yet, your bank account remains stuck in limbo while your own overheads, payroll, and supplier costs keep knocking on the door. If this sounds familiar, you are definitely not alone. Managing day-to-day cash flow is a massive hurdle for thousands of growing businesses across the UK.

Thankfully, you don’t have to just sit around twiddling your thumbs waiting for BACS transfers to land. Forward-thinking companies regularly turn to capital injection strategies to unlock their trapped cash instantly.

Navigating the commercial market can feel overwhelming with all the industry jargon thrown around. In this guide, we will cut through the noise and break down the best invoice finance options UK so you can identify the perfect match for your business model.

The Core Choices: Types of Invoice Finance UK

At its heart, invoice funding is an incredibly simple concept: a specialist lender advances you a significant percentage of your unpaid invoice value (usually around 80% to 95%) almost as soon as you raise it.

Once your customer eventually pays the outstanding bill, the lender releases the remaining balance, minus a small administrative fee. It acts as a highly customisable cash bridge that scales automatically alongside your sales volume.

However, the exact mechanics depend entirely on the specific arrangement you set up. The three main types of invoice finance UK providers offer are Invoice Factoring, Invoice Discounting, and Single/Spot Invoice Finance.

Each layout has distinct operational differences regarding credit control management, privacy, and long-term contractual commitments.

Unlike rigid traditional overdrafts or fixed business loans, invoice funding grows natively with your revenue. The more sales you secure, the more operating capital becomes instantly available to deploy.

Invoice Factoring vs Discounting: The Full-Facility Showdown

When business owners start evaluating comprehensive commercial funding plans, the debate almost always boils down to one fundamental comparison: invoice factoring vs discounting.

While both financial setups achieve the same primary goal, turning unpaid sales sheets into immediate working capital, they approach customer relationships and credit control from opposite sides of the spectrum.

1. Invoice Factoring: Built-In Credit Control

Invoice Factoring is an all-inclusive, fully managed funding facility. When you partner with a factor provider, they don’t just advance you cash; they actively take over your sales ledger administration and debt collection processes.

- Their professional credit control teams will manage customer relations, send out payment reminders, and pick up the phone to chase up overdue accounts on your behalf.

- This structure makes factoring incredibly popular among ambitious start-ups and rapidly growing small-to-medium enterprises (SMEs) that lack a dedicated internal accounts team. It frees up your valuable hours so you can focus entirely on operations and sales.

The main trade-off to keep in mind is transparency: your customers will know you are using a finance provider, as they will interact directly with the factor’s collection staff.

2. Invoice Discounting: Confidential Cash Injection

Invoice Discounting, on the other hand, is a completely confidential funding arrangement designed for established companies with functional in-house finance operations.

- With this facility, the lender still advances cash against your outstanding ledger, but your internal credit control team retains total control over debt collection. Your customers will never know a third-party finance company is involved.

- They continue paying into a designated trust bank account under your company’s name. It offers a seamless, discreet way to inject capital without changing how your customer relationships feel on the ground.

Because the lender takes on a bit more structural risk by trusting your team to collect the money, they typically require a higher annual turnover baseline to qualify.

What is Spot Invoice Finance and How Does It Work?

Full-facility factoring and discounting plans are fantastic, but they usually require you to sign a contract covering your entire sales ledger for 12 to 24 months. But what if you don’t want to commit your whole business to a long-term contract?

- What if you only need a temporary boost to handle a single massive order or bridge a seasonal gap? This is where spot invoice finance UK solutions come into play.

- Often referred to as selective invoice finance, this ultra-flexible setup allows you to fund an individual invoice or a specific customer account whenever you choose, completely free from ongoing contractual obligations.

- The operational process is wonderfully simple: you pick a high-value invoice from a reliable client, upload it to an online spot provider’s portal, and receive the cash advance within 24 hours. Once the customer settles that specific bill, the transaction closes out cleanly.

It acts as an on-demand, highly tactical tool that delivers flexible business finance UK companies can activate exactly when they need it most, without dragging along a trail of recurring monthly fees.

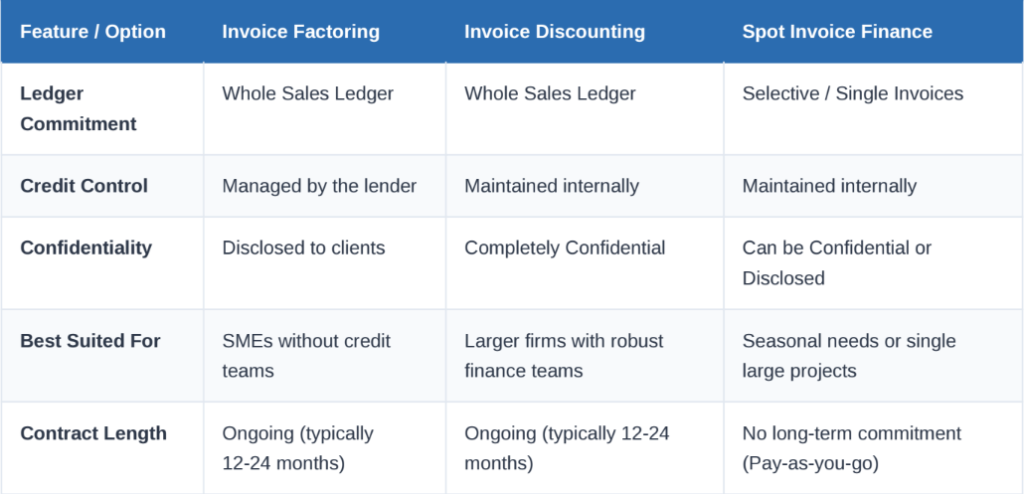

Invoice Funding Comparison: At a Glance

To help you visualise how these three popular funding frameworks match up, we’ve put together a straightforward comparison matrix covering the key features businesses care about most:

How Do I Choose Between Invoice Finance Options?

Finding the absolute best setup for your company isn’t about looking for a one-size-fits-all answer; it’s about matching a facility to your operational realities. To figure out the right path forward, take a moment to look at your business through these three simple lenses:

- In-House Capabilities:

Do you have the spare time and staff to chase up late payments? If yes, confidential discounting keeps you in the driver’s seat. If your team is already stretched thin, letting a factoring company handle credit control can save you a massive headache.

- Client Relationships:

Are you worried about how your corporate clients might react to seeing a third-party financier on your paperwork? If keeping things discreet is a top priority, a confidential arrangement is definitely the way to go.

- Consistency of Cash Needs:

Is your working capital gap a constant hurdle, or does it pop up randomly? Regular, predictable shortfalls are best solved by full ledger facilities, while irregular, project-based gaps are perfect for spot funding.

Summary: Unlocking Your Business Potential

At the end of the day, cash flow shouldn’t hold back your business growth. By taking a close look at the best invoice finance options UK lenders provide, you can transform your unpaid customer bills into an active source of growth capital.

Whether you choose the comprehensive credit management of factoring, the quiet discretion of discounting, or the pay-as-you-go freedom of spot finance, you’re putting yourself back in control of your financial destiny.

Ans:- There is no single “best” type; it depends entirely on your setup. Factoring is perfect for small businesses needing credit control assistance, invoice discounting works beautifully for larger firms wanting confidentiality, and spot finance is best for flexible, occasional use.

Ans:- Neither is universally better, but established businesses typically prefer discounting because it keeps the financing completely confidential from clients and allows you to retain total internal control over your credit relationships.

Ans:- Spot invoice finance is an on-demand funding solution where you sell a single invoice to a lender for an immediate cash advance. Once your customer pays that specific invoice, the balance is released, and the agreement ends.

Ans:- Invoice discounting is usually the cheapest option on a per-invoice basis because the lender doesn’t manage credit collection. However, spot finance can be more cost-effective overall if you only need funding for a few times a year.

Ans:- Analyse your annual turnover, check if you have an internal credit control team to chase invoices, and decide if you need a long-term facility for your whole ledger or just flexible, transactional cash injections for single bills.

Discover the Latest Trends

Stay informed with our latest articles and resources.