Invoice Discounting Services: What UK Businesses Need to Know in 2026

Running a business in the UK can often feel like a juggling act. You’ve got the orders coming in, the team is working hard, and the vision is there. But then you look at your bank balance and realise all your hard-earned cash is currently sitting in a “Pending” pile on someone else’s desk.

Late payments are a classic British business headache. Whether you’re a recruitment agency, a logistics firm, or a manufacturer, waiting 30, 60, or even 90 days for a client to settle up can seriously stall your momentum. This is where invoice discounting services enter the chat.

Think of it as a way to “unlock” the money you’ve already earned without waiting for the slow-motion wheels of corporate finance to turn.

Let’s break down what this service actually is, how it works in the UK, and why it might be the secret weapon your cash flow needs.

What is Invoice Discounting?

Invoice discounting services are a type of business finance that lets you borrow money against your unpaid invoices. Instead of waiting for a client to pay you in three months, a finance provider gives you a considerable amount of that money (around 80% to 95%) almost immediately, often within 24 hours of you raising the invoice.

The “Secret” Difference

People often confuse Invoice Discounting with Invoice Factoring. While they are cousins, they aren’t twins. The biggest “pro” for discounting is confidentiality.

With factoring, the finance company usually takes over your “credit control” (meaning they’re the ones calling your clients to chase payments).

With invoice discounting, you stay in the driver’s seat. You keep chasing the payments, your customers pay into a bank account in your name, and they never even have to know you’re using a finance service. It’s the ultimate “stealth mode” for managing cash flow.

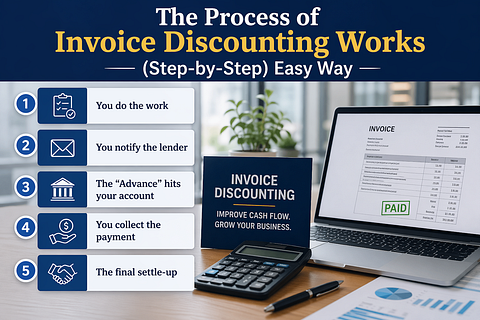

How the Process Works (Step-by-Step) in Easy Way

If you’re a UK business owner, the process is actually surprisingly fast:

- You do the work: You sell your goods or services to another business and send them an invoice as usual.

- You notify the lender: You send a copy of that invoice to your invoice discounting provider.

- The “Advance” hits your account: The provider sends you a percentage of the invoice value (e.g., 90%) right away.

- You collect the payment: You manage your relationship with the client, and they pay you on their usual terms.

- The final settle-up: Once the client pays, you pay the lender back, and they release the remaining 10% to you, minus a small fee for their service.

Is Your Business a Good Fit?

While it sounds like a dream, invoice discounting services aren’t for everyone. UK lenders typically look for businesses that meet a few criteria:

- B2B Sales: This is for businesses selling to other businesses. If you’re a high-street shop selling to the general public, this won’t work for you.

- Established Track Record: Lenders like to see a bit of history. Most providers look for a turnover of at least £100,000 to £250,000 per year.

- Solid Credit Control: Because you are responsible for chasing the money, the lender needs to trust that your internal finance team knows how to get paid.

The Costs: What’s the Damage?

Nobody gives out money for free, unfortunately! When looking at invoice discounting services, you’ll generally see two types of fees:

- Service Fee: This is basically the “subscription” cost. It covers the administration of the facility and is usually a small percentage of your annual turnover (often between 0.2% and 0.5%).

- Discount Fee: Think of this as the interest. It’s charged on the money you actually draw down and is usually tied to the Bank of England base rate plus a small margin (typically 1.5% to 3%).

For many UK SMEs, these costs are a small price to pay compared to the cost of a missed opportunity or a stalled project because the cash wasn’t there.

The Pros and Cons of Invoice Discounting Services in 2026

| Pros of Invoice Discounting Services | Cons of Invoice Discounting Services |

| Instant Cash: Get paid in 24 hours instead of 60 days. | Responsibility: You still have to chase the late payers. |

| Confidential: Your clients don’t know you’re using it. | Eligibility: Harder for brand-new startups to access. |

| Flexible: The more you sell, the more cash you can unlock. | Cost: It’s more expensive than a standard bank loan. |

| Control: You keep managing your own customer relationships. | Risk: If a client goes bust, you might still owe the lender. |

Also Read:- Single Invoice Discounting: A Smart Funding Option for Growing Businesses

Final Thoughts

Invoice discounting isn’t just about “fixing” a problem; it’s about fueling growth. If you find yourself turning down new contracts or delaying a big equipment purchase because you’re waiting on a check from a “slow-paying” corporate client, this could be the bridge you need.

In the UK’s fast-moving market, cash is king and invoice discounting services let you keep the crown. Would you like me to help you compare a few UK-based providers to see which one fits your industry best?

FAQs

Q. Will my customers know I’m using an invoice discounting service?

Ans:- Usually, no! One of the main reasons UK businesses choose discounting over factoring is confidentiality. You continue to manage your own sales ledger and chase payments, so the relationship between you and your client stays the same.

Q. Can I choose which invoices to discount?

Ans:- It depends on your agreement! “Whole Ledger” discounting means you use the service for all your invoices. However, many providers offer “Selective” or “Spot” discounting, where you can pick and choose specific high-value invoices to unlock when you need a boost.

Q. What happens if my customer doesn’t pay?

Ans:- Most standard agreements are “Recourse,” meaning if your client doesn’t pay, you have to pay the lender back yourself. However, you can opt for “Non-Recourse” discounting (often called Bad Debt Protection), where the lender takes on the risk if your client goes insolvent.

Q. How is this different from a bank loan?

Ans:- A bank loan is a fixed amount of debt that stays on your balance sheet. Invoice discounting services by Best Invoice Finance are a revolving facility that grows as your business grows. You aren’t “borrowing” in the traditional sense; you’re just accessing your own money earlier.

Q. How long does it take to set up?

Ans:- Unlike a traditional bank loan, which can take weeks of paperwork, a UK invoice finance provider can often have your facility set up and your first payment in your account within 5 to 10 working days.

Discover the Latest Trends

Stay informed with our latest articles and resources.