Struggling with Seasonal Cash Flow? How Invoice Finance Keeps Your Business Stable

Running a business is often less like a smooth highway and more like a rollercoaster. One month, you’re at the peak, orders are flying in, the team is buzzing, and the revenue looks fantastic. The next? You’ve hit a dip. The phone is quiet, but the bills, rent, payroll, and utilities don’t care that it’s your “off-season.”

If your business experiences these peaks and valleys, you’re dealing with seasonal cash flow problems. It’s a common headache, especially for industries like retail, tourism, or construction. The irony is that being “busy” can sometimes be the hardest part, as you spend a fortune upfront to fulfil orders but wait 30, 60, or even 90 days actually to get paid.

This is where invoice finance for cash flow enters the chat. It’s the business equivalent of an espresso shot for your bank account, quick, effective, and designed to keep you moving when you’d otherwise be stalled.

Why Do Businesses Face Seasonal Cash Flow Problems?

It usually comes down to a timing mismatch. Think of a landscaping company. In the spring and summer, they are hiring extra staff and buying bulk materials. They do the work, send the invoice, and then… they wait. Meanwhile, they still have to pay their suppliers and workers.

Seasonal cash flow problems happen because your expenses are often “upfront” while your income is “delayed.” If your business relies on a specific time of year, like Christmas or the summer holiday season, you have to spend a massive amount of capital to prepare for that.

If your customers are slow to pay their invoices during the transition into the slower months, you find yourself with a “black hole” in your budget. You’re profitable on paper, but your bank account is empty. That’s a dangerous place to be.

How Does Invoice Finance Improve Cash Flow?

Instead of waiting for a client to finally click “pay” on an invoice, invoice finance for cash flow lets you unlock that money almost immediately. Here’s the simple version of how it works:

- You finish a job and send an invoice to your customer.

- You “sell” or assign that invoice to a finance provider.

- The provider gives you a huge chunk of that invoice value (often up to 90%) within 24 hours.

- Once your customer pays the invoice, the provider gives you the remaining balance, minus a small fee.

It basically turns your “Accounts Receivable” into actual, spendable cash. You aren’t taking on a traditional loan that sits on your balance sheet for years; you’re simply getting an advance on money that already belongs to you. It’s one of the most flexible ways to manage business cash flow because the amount of funding grows alongside your sales.

How to Stabilise Cash Flow Using Invoice Finance?

To stabilise cash flow using invoice finance, you need to stop viewing it as an “emergency” measure and start seeing it as a strategic tool. By having an invoice finance facility in place, you create a “smoothing” effect. During your busiest months, when you are issuing hundreds of invoices, your available cash increases instantly.

It allows you to pay your suppliers early (sometimes even snagging an early-payment discount!) and keep your working capital support levels high. You no longer have to turn down a big new contract just because you’re worried about how you’ll fund the initial costs.

Can Invoice Finance Help During Slow Seasons?

While invoice finance relies on having active invoices to “fund,” it helps during slow seasons by ensuring you enter that period with a healthy cash reserve.

If you use an invoice finance solution during your peak months, you can build up a cash cushion rather than spending every penny on immediate overheads.

Furthermore, as the last of your big peak-season invoices come in, you can liquidate them instantly to cover the fixed costs (like rent and core staff) that persist even when sales have slowed down. It acts as a bridge, ensuring the “dry” months don’t result in a total drought.

Which Industries Benefit Most From Invoice Finance?

While almost any B2B company can use it, certain sectors find it life-saving:

- Transport & Logistics: Fuel and maintenance don’t wait for 30-day invoice cycles.

- Wholesale & Distribution: High inventory costs and long payment terms make this a prime candidate.

- Recruitment: You have to pay your contractors weekly, but your clients might pay you monthly. Invoice finance fills that gap perfectly.

- Manufacturing: Raw materials are expensive. Getting cash flow funding against finished goods invoices helps keep the production line moving.

The Big Picture: Beyond the “Quick Fix”

Many business owners get nervous about the word “finance.” They think it means the business is struggling. In reality, the most successful companies in the world use debt and financing strategically to grow faster. Using invoice finance for cash flow isn’t about “saving” a failing business; it’s about empowering a growing one.

Invoice finance services from Best Invoice Finance give you the confidence to say “yes” to new opportunities. When you aren’t constantly checking the bank balance to see if a specific check has cleared, you can focus on what you actually enjoy: strategy, sales, and building your brand.

It provides a level of working capital support that traditional bank loans simply can’t match. A bank loan is a fixed amount; invoice finance is elastic. As your business grows and you send more invoices, your “credit limit” effectively grows with you. It’s a dynamic way to manage business cash flow that stays in sync with your actual performance.

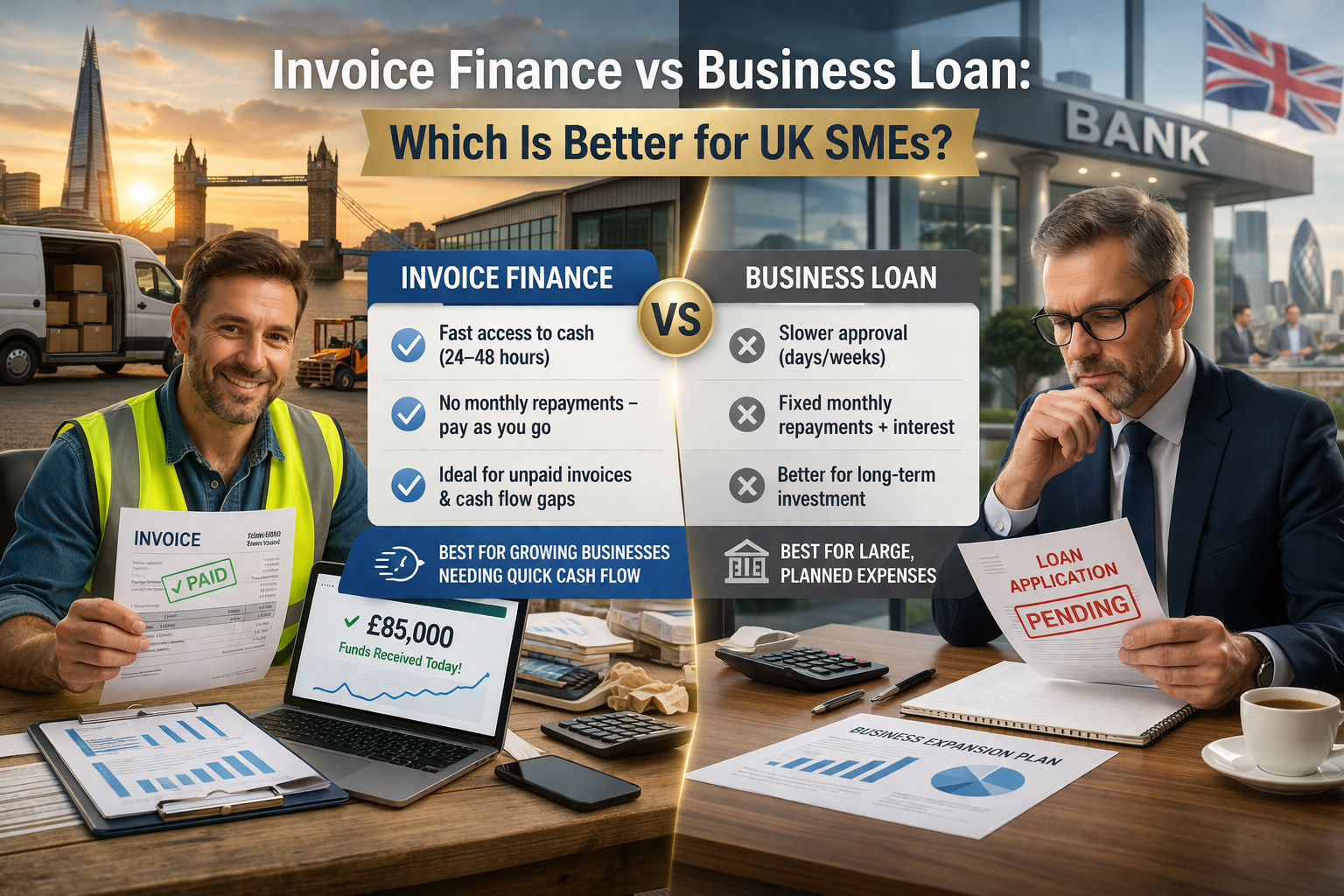

Also Read:- Invoice Finance vs Business Loan: Which Is Better for UK SMEs?

Conclusion

Managing the “ebbs and flows” of a seasonal business doesn’t have to be a source of constant stress. By using invoice finance for cash flow, you can take control of your timing, protect your team, and ensure that your business remains stable 365 days a year—not just when the sun is shining.

FAQs

Q. Is invoice finance the same as a bank loan?

Ans:- Not exactly. A bank loan involves borrowing a lump sum and paying it back with interest over time. Invoice finance is an advance based on your outstanding invoices. It’s much more flexible and doesn’t usually require collateral.

Q. Will my customers know I’m using an invoice finance provider?

Ans:- It depends on the type you choose. With “Invoice Factoring,” the provider often handles the collections, so that the customer will know. However, with “Invoice Discounting,” the arrangement is typically confidential.

Q. What are the costs associated with this type of cash flow funding?

Ans:- Usually, there are two main costs: a service fee (for managing the facility) and a discounting fee (similar to an interest rate on the money you actually draw down). For many, these costs are easily offset by the ability to take on more work or negotiate better prices with suppliers.

Q. How long does it take to set up an invoice finance facility?

Ans:- While a bank loan can take weeks or even months of paperwork, an invoice finance facility can often be up and running in 5 to 10 working days. Once it’s set up, individual invoices can be funded within 24 hours of being uploaded.

Q. Can small businesses or startups use invoice finance?

Ans:- Yes! As long as you are a B2B business and you have creditworthy customers, you can often find a provider. Many providers specifically tailor their services to SMEs that need a bit of extra help to jump-start their growth.

Discover the Latest Trends

Stay informed with our latest articles and resources.