Growing Too Fast? How Invoice Finance Supports Business Expansion Without Cash Shortage

Imagine your sales are skyrocketing, your client list is stretching off the page, and everyone wants a piece of what you’re selling. But then, you look at your bank account and realise something terrifying: you’re actually running out of money.

Welcome to the paradox of the “growth trap.” Scaling a business is expensive. You need more stock, more staff, and bigger premises long before the checks from those new sales actually clear. If you aren’t careful, you can literally outgrow your bank balance.

This is where invoice finance for business growth becomes the secret weapon for savvy owners who want to keep the momentum without hitting a wall.

Why Do Fast-Growing Businesses Face Cash Shortages?

It feels counterintuitive. If you’re selling more, you should have more money, right? In reality, growth is a hungry beast. To fulfil a massive new contract, you might have to pay suppliers today, cover an increased payroll on Friday, and invest in new equipment this month.

However, your big corporate clients might operate on 30, 60, or even 90-day payment terms. It creates a massive need for a cash flow gap solution.

You are essentially acting as a bank for your customers, lending them money in the form of goods or services while your own coffers run dry. Without a bridge to cover that gap, your expansion can grind to a halt just as it’s getting started.

The “Wait Problem”: Solving the Cash Flow Gap

The traditional way to handle growth was to bootstrap and wait for the money to come in. But in today’s market, waiting is a luxury you can’t afford. If you don’t pounce on an opportunity, your competitor will.

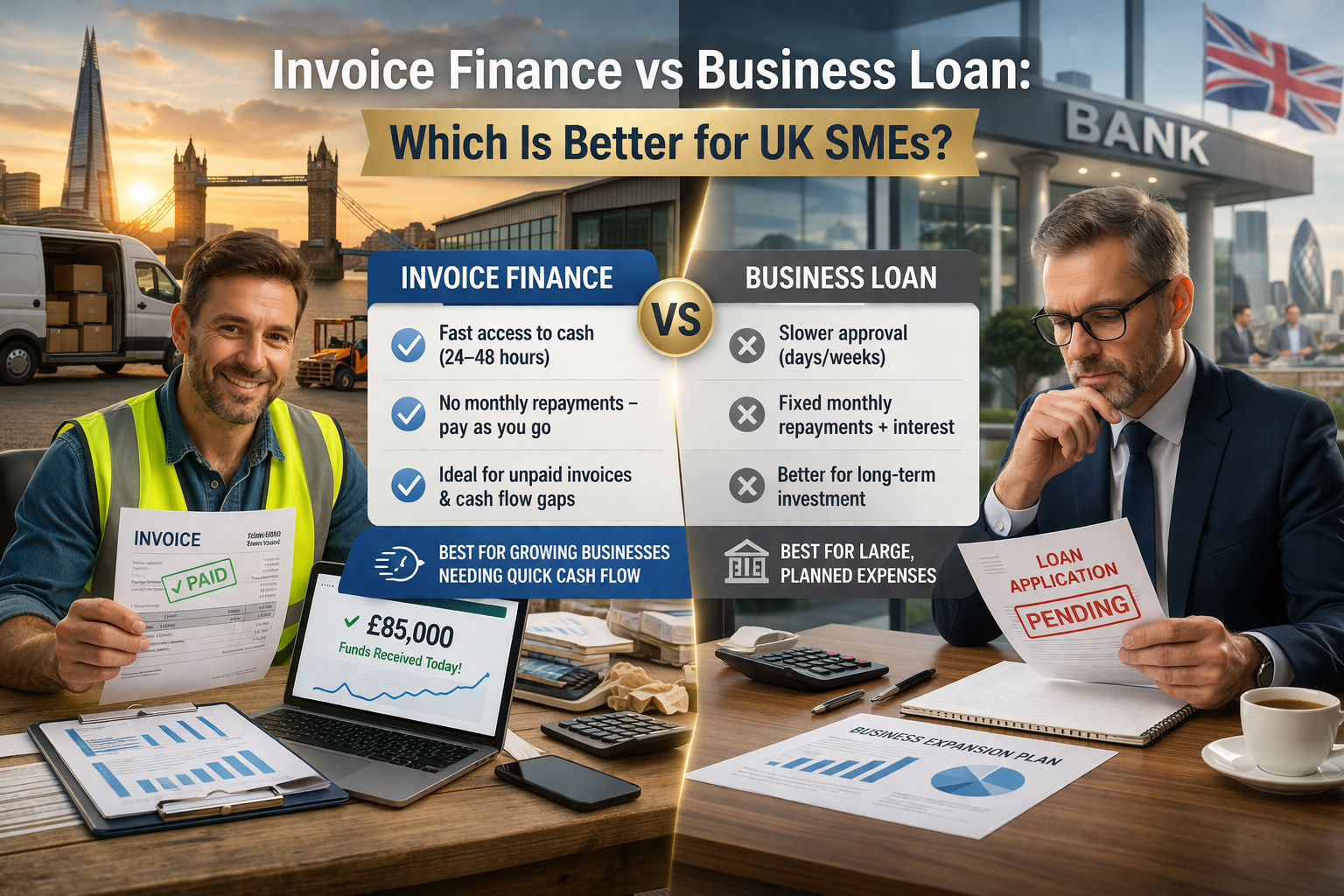

Invoice finance for business growth flips the script. Instead of waiting months for a client to pay, a finance provider advances you a significant percentage (often up to 90%) of the invoice value within 24 hours of you raising it.

When the client eventually pays, you get the remaining balance, minus a small fee. It’s your own money, just unlocked early. It turns your accounts receivable into immediate working capital for expansion.

Can Invoice Finance Replace Traditional Loans?

For many scaling companies, the answer is a resounding yes. Traditional bank loans are often rigid. You borrow a set amount, pay it back over a fixed term, and if you suddenly grow faster than expected, you have to go back through the hectic application process all over again.

Invoice finance is different because it’s “elastic.” As your sales grow, your available funding grows automatically. If you invoice $100k this month, you can access $90k.

If you grow to $500k next month, your funding limit scales right along with you. It’s a dynamic form of finance for growing business that doesn’t require you to take on the heavy, fixed debt of a standard term loan.

How to Maintain Cash Flow While Growing?

Maintaining a healthy pulse in your business while scaling business cash flow requires a multi-pronged approach:

- Tighten Credit Control: Don’t be afraid to chase late payers. Clear communication is key.

- Use Technology: Automated invoicing ensures no time is lost between finishing a job and sending the bill.

- Negotiate with Suppliers: If your clients pay in 60 days, try to get your suppliers to give you 60-day terms too.

- Leverage Asset Power: Using your invoices as collateral ensures that your capital isn’t “trapped” in a filing cabinet waiting for a due date.

What are the Risks of Scaling Without Funding?

Trying to grow purely on “hope and grit” is risky. The biggest danger is “overtrading”—taking on more work than you have the cash to support. If one major client pays late, it can trigger a domino effect.

You might miss your own supplier payments, damaging your reputation, or worse, struggle to meet payroll. It creates a “growth plateau” where you have to turn down new orders because you simply can’t afford to fulfil them.

Having a dedicated cash flow gap solution by Best Finance Invoice in place acts as a safety net, allowing you to say “yes” to big opportunities with confidence.

Also Read:- Struggling with Seasonal Cash Flow? How Invoice Finance Keeps Your Business Stable

Final Thoughts: Fueling the Fire

Expansion is an exciting time, but it’s also the most vulnerable period for any company. By using invoice finance for business growth, you aren’t just “surviving” the wait for payment; you’re weaponising your sales.

You’re taking the money you’ve already earned and putting it back to work immediately, hiring that next specialist, buying that next pallet of raw materials, and keeping the engine humming. Growth shouldn’t be a gamble. With the right funding structure, it’s just the next logical step.

FAQs

Q:- How does invoice finance support expansion?

Ans:- It provides immediate access to cash tied up in unpaid invoices. It allows you to reinvest in staff, inventory, and marketing without waiting 30–90 days for clients to pay.

Q:- Is my business too small for invoice finance?

Ans:- Not at all. Many providers work with startups and SMEs. As long as you are B2B and have creditworthy customers, it’s a viable way to scale business cash flow.

Q:- Does my client know I’m using invoice finance?

Ans:- It depends! With “Invoice Factoring,” the provider handles collections, and your client knows. With “Invoice Discounting,” the arrangement is usually confidential, and you keep managing your own credit control.

Q:- Is it expensive compared to a bank overdraft?

Ans:- While there are fees involved, it is often more cost-effective than an unauthorised overdraft or the “opportunity cost” of turning down a massive new contract because you lack the funds.

Q:- What happens if a customer doesn’t pay?

Ans:- Most agreements are “recourse,” meaning you’re responsible if the client defaults. However, you can opt for “Non-Recourse” finance, which includes bad debt protection to keep your working capital for expansion safe.

Discover the Latest Trends

Stay informed with our latest articles and resources.