Single Invoice Finance UK: How to Fund One Invoice Without Long-Term Contracts

Running a business in the UK often feels like a balancing act. You’ve done the work, your client is happy, and you’ve sent off a healthy invoice. But then comes the wait. Whether it’s a 30, 60, or even 90-day payment term, that gap can put a serious dent in your cash flow.

Historically, if you wanted help from a bank, they’d try to lock you into a “whole turnover” agreement, meaning they’d want a piece of every single invoice you issued for the next year. But what if you only need a boost for one specific project?

Enter single invoice finance UK. It’s the flexible version of business funding that’s changing the game for SMEs.

Can I Finance Just One Invoice in the UK?

Yes, absolutely. You don’t have to commit your entire sales ledger to a finance provider anymore. This modern approach is often called spot invoice finance UK.

Spot invoice finance is designed for businesses that generally have healthy cash flow but occasionally hit a “bump” or a big opportunity that requires immediate capital.

Maybe you’ve just landed a massive contract and need to buy raw materials, or perhaps a large client has pushed back their payment date, leaving you tight on payroll. In these scenarios, you can pick a single, high-value invoice and turn it into cash today.

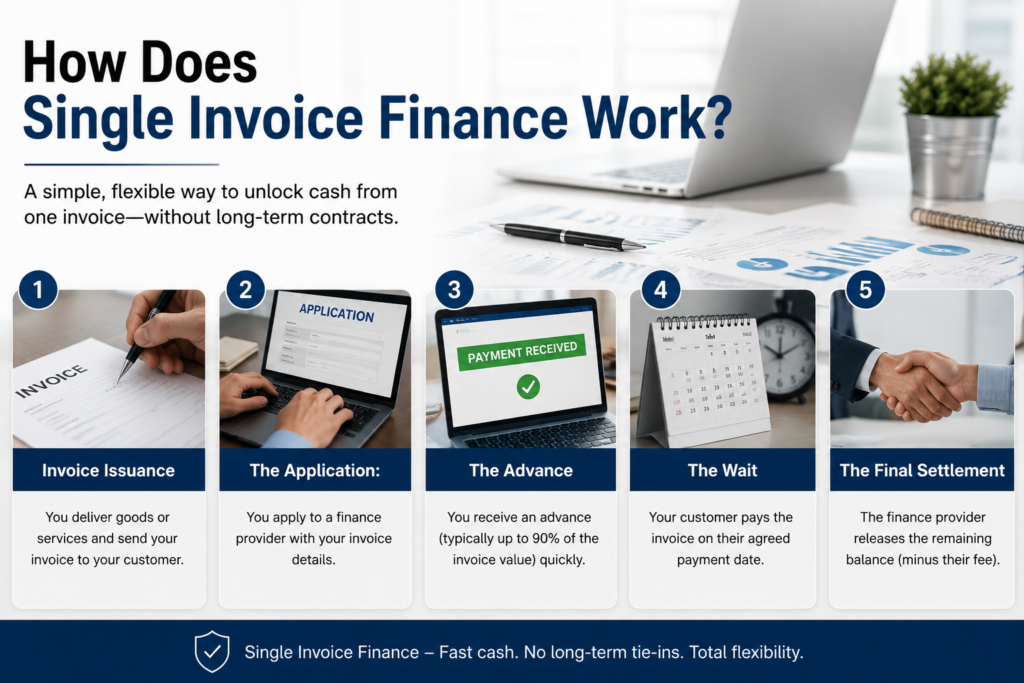

How Does Single Invoice Finance Work?

The process is surprisingly straightforward and built for speed. If you’ve never used single or selective invoice finance before, here is the typical step-by-step process:

- Invoice Issuance: You complete your work and send the invoice to your customer as usual.

- The Application: You “sell” that specific invoice to a finance provider.

- The Advance: The provider verifies the invoice and sends you a significant percentage of its value (usually 80% to 90%) within 24 hours.

- The Wait: Your customer pays the invoice according to their original terms, but they pay it into a dedicated account controlled by the lender.

- The Final Settlement: Once the customer pays in full, the lender sends you the remaining balance, minus a small fee for the service.

Do I Need a Contract for Invoice Finance UK?

One of the biggest hurdles with traditional factoring is the paperwork and the long-term commitment. However, with invoice funding without contract requirements, you are in the driver’s seat. Most “spot” or “selective” providers operate on a “pay-as-you-go” basis.

You sign up for a master agreement once, which acts as a framework, but you are under no obligation to use the facility. You only pay when you actually fund an invoice.

This short term invoice finance model is perfect for seasonal businesses or those with sporadic, large-scale projects.

Is Spot Invoice Finance Better Than Factoring?

Whether single invoice finance UK is “better” or not depends entirely on your business model.

- Factoring is great if you want someone to take over your entire credit control and provide a steady stream of cash for every sale. It’s a long-term partnership.

- Spot Invoice Finance is superior if you value independence. You keep control of your customer relationships, you don’t pay “minimum monthly fees,” and you only use the service when it makes financial sense for a specific situation.

For many UK business owners, the transparency of one invoice funding is the winner because it doesn’t clutter the balance sheet with long-term debt.

How Fast Can I Get Paid for One Invoice?

In the world of business, “speed is a feature.” Traditional bank loans can take weeks of back-and-forth. With single invoice finance UK, the timeline is usually measured in hours.

Once your account is set up, most providers can verify an invoice and move funds into your business account on the same day. This makes it an invaluable tool for emergency repairs, tax bills, or seizing a “limited time” discount from one of your own suppliers.

How Best Invoice Finance Can Help?

Navigating the UK’s financial landscape can be overwhelming. There are dozens of lenders, all with different fee structures and “hidden” small print. This is where Best Invoice Finance steps in. As experts in the UK market, Best Invoice Finance acts as your bridge to the right lenders.

They specialise in finding selective invoice finance solutions that match your specific industry and client base. Instead of you spending hours calling different banks, they use their network to find the most competitive rates and the most flexible terms.

Whether you are looking for a one-off “spot” facility or a slightly more regular selective arrangement, they ensure you aren’t overpaying for your cash flow.

Also Read:- Invoice Discounting Rates in the UK: What Businesses Really Pay & How to Reduce Costs

The Verdict: Flexibility is King

- The UK economy moves fast, and your funding should move faster. Single invoice finance UK offers the ultimate “safety net” without the “trap” of a three-year contract. It allows you to leverage your own hard work, your invoices, to fund your future growth.

Ready to Unlock Your Cash Flow?

- Don’t let unpaid invoices hold your business back. Whether you need to cover a sudden expense or want to invest in a new opportunity, the team at Best Invoice Finance is ready to help you find the perfect funding solution.

Contact Best Invoice Finance Today for a Free Quote.

Ans: Yes. Spot or selective invoice finance allows you to pick and choose individual invoices to fund without committing your entire ledger.

Ans: You sell an unpaid invoice to a lender. They give you ~90% of the cash immediately. When the customer pays, you get the rest, minus a fee.

Ans: It’s better for flexibility. Unlike factoring, it doesn’t require a long-term contract or a percentage of every sale you make.

Ans: Usually within 24 hours. Once your initial profile is approved, funding is often processed on the same day you submit the invoice.

Ans: For spot finance, you don’t need a “lock-in” contract. You sign a framework agreement and only use it (and pay for it) when you choose to.

Discover the Latest Trends

Stay informed with our latest articles and resources.