Spot Invoice Finance in the UK: Fast Funding for Urgent Cash Flow Needs

Running a business in the UK is not an easy task. One minute you’ve landed a massive contract, and the next, you’re staring at a stack of unpaid invoices while your own bills start to pile up. You have the money, but it’s just sitting in someone else’s bank account for the next 30, 60, or even 90 days.

Traditionally, you might look at a bank loan or a full-blown factoring facility. But what if you don’t want a long-term commitment? What if you just have that one high-value invoice that’s keeping you up at night? That’s where spot invoice finance enters the chat. It’s the flexible version of business funding that’s becoming a lifesaver for UK SMEs.

What is Spot Invoice Finance, and How Does It Work?

Think of spot finance (also known as single invoice discounting) like a “pay-as-you-go” service for your cash flow. Instead of signing over your entire sales ledger to a finance company, which is what happens with traditional factoring, you pick and choose which individual invoices you want to turn into cash immediately. The process is pretty simple:

- You finish a job and send the invoice to your client as usual.

- You “sell” that specific invoice to a quick invoice funding UK provider.

- The provider advances you a significant chunk of the invoice value (usually around 80% to 90%) almost immediately.

- Once your customer pays the invoice, the finance provider sends you the remaining balance, minus a small fee for their trouble.

It’s a surgical strike on cash flow gaps. You get the money you’ve already earned without waiting for the customer’s accounting department to get around to pressing “send.”

Why It’s the Instant Invoice Finance Solution UK Businesses Love?

The biggest draw here is speed and control. In the fast-paced UK market, opportunities don’t wait. Maybe you need to buy stock for a surprise order, or perhaps you need to cover a tax bill.

How quickly can I get funds with spot invoice finance in the UK?

- In many cases, once you’re set up with a provider, you can see the money in your account within 24 hours. Some modern fintech platforms can even process it in a matter of hours.

- Compare that to a traditional bank loan that might take weeks of paperwork and “computer says no” moments, and it’s easy to see why it’s called an instant invoice finance solution.

Is Spot Invoice Finance Expensive Compared to Other Options?

As you aren’t committing to a long-term contract, the “per-invoice” fee for spot invoice finance can be slightly higher than the rates you’d get on a whole-ledger facility.

However, you have to look at the “hidden” costs of other options. With traditional factoring, you might pay monthly admin fees, non-utilisation fees, and exit fees, even if you don’t need to fund every invoice.

With the spot model, you only pay when you use it. If you only have a cash flow gap twice a year, spot finance is almost certainly the cheaper, more logical choice. You aren’t paying for a service you don’t need 90% of the time.

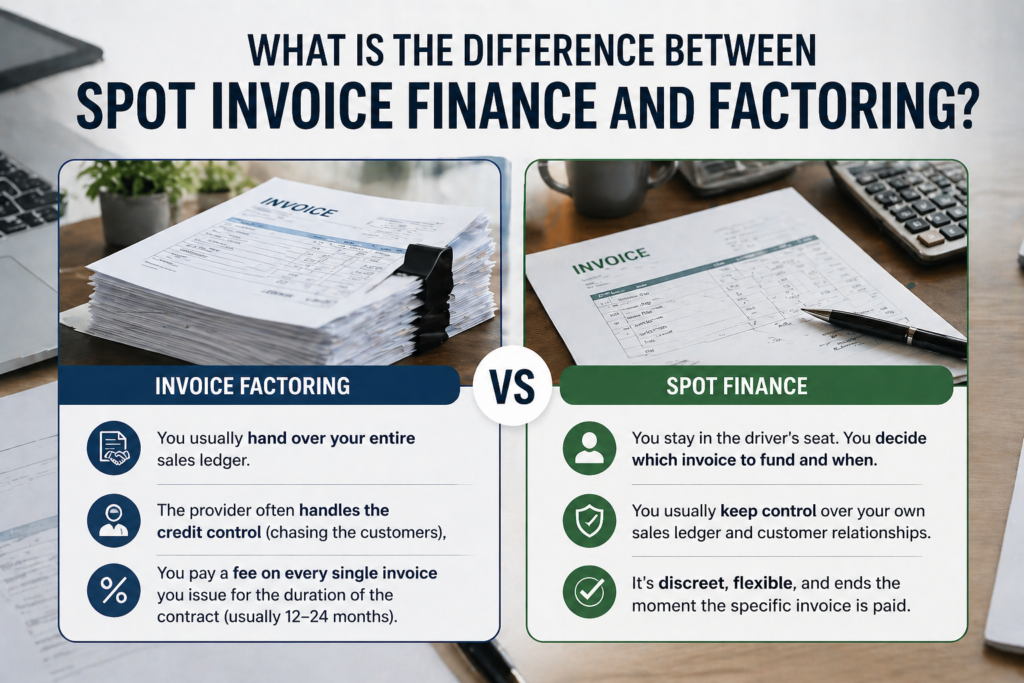

What is the Difference Between Spot Invoice Finance and Factoring?

It really comes down to commitment and volume.

- Invoice Factoring: You usually hand over your entire sales ledger. The provider often handles the credit control (chasing the customers), and you pay a fee on every single invoice you issue for the duration of the contract (usually 12–24 months).

- Spot Finance: You stay in the driver’s seat. You decide which invoice to fund and when. You usually keep control over your own sales ledger and customer relationships. It’s discreet, flexible, and ends the moment the specific invoice is paid.

Can Startups Use Spot Invoice Finance?

Absolutely. In fact, it’s one of the best tools for a growing business. Spot invoice finance UK providers are often more interested in the creditworthiness of your customer (the one paying the invoice) than in the length of your trading history.

If you’re a startup that has just landed a contract with a reputable, blue-chip company or a government body, a finance provider will be very happy to advance you the cash because they know the end-payer is reliable. It’s a great way to fuel growth without giving up equity or taking on debt that sits on your balance sheet forever.

Finding the Right Partner: Best Invoice Finance

If you’re looking into this, you’ll want a partner that understands the UK landscape. Best Invoice Finance specialises in helping businesses navigate these waters. We don’t just look at you as a number on a spreadsheet; we help match your specific business needs with the right funding structure.

Whether you’re looking for a one-off boost or a more regular arrangement, having an expert like Best Invoice Finance in your corner ensures you aren’t overpaying and that the funds arrive exactly when you need them.

Also Read:- Selective Invoice Finance UK: Choose Which Invoices to Fund and Improve Cash Flow

Final Thoughts

Cash flow shouldn’t be the thing that kills a good business. If you have solid customers but a slow bank balance, spot invoice finance is the modern way to bridge the gap. It’s fast, it’s flexible, and it puts you back in control of your business growth.

FAQs

Q. Do my customers need to know I’m using spot invoice finance?

Ans:- Not necessarily. Many providers offer “confidential” options where the facility is invisible to your clients, allowing you to maintain your usual branding and communication.

Q. Is there a minimum invoice value required?

Ans:- It varies by provider, but many quick invoice funding UK services handle invoices as small as £1,000, while others focus on much larger six-figure sums.

Q. What happens if my customer doesn’t pay?

Ans:- It depends on whether you have “recourse” or “non-recourse” finance. With recourse, you are responsible for the debt if the client fails to pay. Non-recourse includes insurance to protect you if the client goes bust.

Q. Can I use it for international customers?

Ans:- Yes, many UK providers can fund invoices for overseas clients, provided they are in approved countries and trade in major currencies.

Q. How do I apply?

Ans:- Usually, you just need your company details, a copy of the invoice you want to fund, and evidence that the work has been completed or the goods delivered. The setup is designed to be quick and digital.

Discover the Latest Trends

Stay informed with our latest articles and resources.