Invoice Finance for Retail Businesses: How It Improves Cash Flow

Ever walked into a bustling retail store, saw all those shelves stocked with the latest trends, and thought, “Wow, they must be making a killing!”? Well, the truth is, behind every well-stocked shelf and successful sales season in the UK, there’s often a silent battle being fought: the battle for cash flow.

For retail businesses, especially those supplying to larger chains or operating on wholesale terms, the gap between selling goods and actually getting paid can feel like an endless desert. You’ve invested in inventory, paid your staff, covered your rent – but the money from that big order you shipped last month? Still waiting.

This is where invoice finance for retail businesses steps in, transforming those “waiting periods” into immediate cash. It’s less about traditional loans and more about unlocking the value already sitting in your unpaid invoices. Let’s dive into how this powerful tool can be a game-changer for UK retailers.

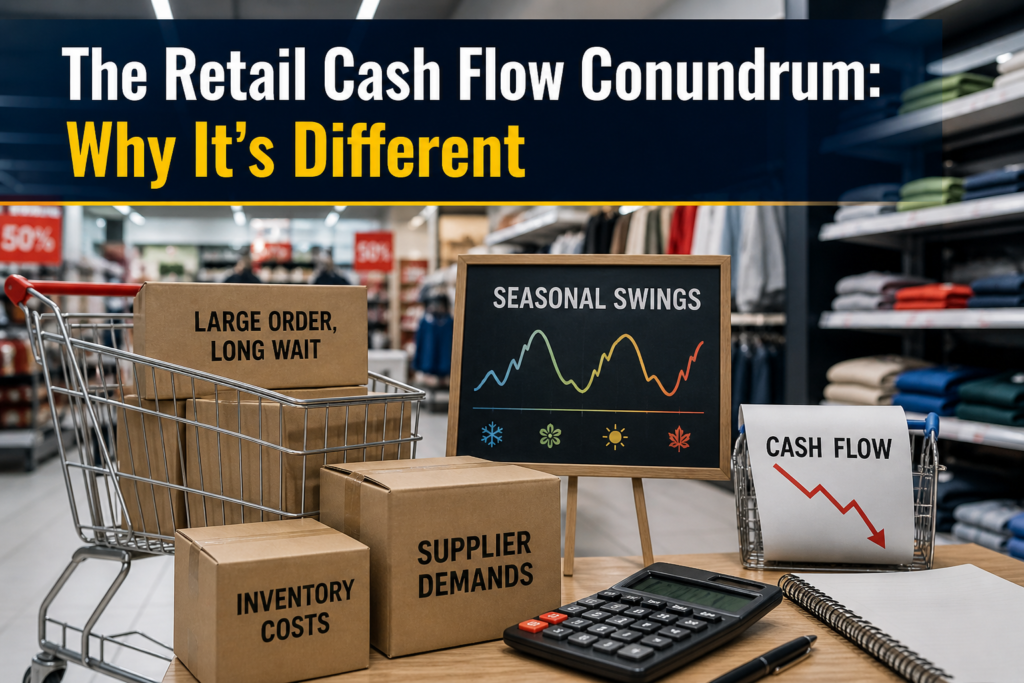

The Retail Cash Flow Conundrum: Why It’s Different

Retail is unique. You’re constantly dealing with:

- Large Order, Long Wait: If you supply to supermarkets, department stores, or even online giants, they often have payment terms of 60, 90, or even 120 days.

- Seasonal Swings: Huge peaks (Christmas, summer sales) followed by troughs. You need cash before the season starts to buy stock.

- Supplier Demands: Many suppliers want upfront payment or very short credit terms.

- Inventory Costs: Your capital is tied up in stock sitting on shelves or in warehouses.

Imagine you’re a fashion brand supplying a major high-street chain. You’ve designed, manufactured, and shipped thousands of units. That’s a huge investment. But the payment from the retailer might not arrive for another two or three months. How do you pay your fabric suppliers, your factory, and your marketing team now? It is the classic retail cash flow trap.

How Invoice Finance Works for Retail Businesses

Invoice finance essentially bridges that cash flow gap. Instead of waiting for your customers to pay, an invoice finance provider gives you an immediate cash advance on your unpaid invoices. Here’s the simple breakdown:

- You Deliver Goods/Services: Your retail business supplies products to a customer (e.g., a supermarket chain, a boutique, an online retailer).

- Get Immediate Cash: The provider advances you a large percentage of the invoice value (typically 80-95%) within 24-48 hours.

- You Get the Rest (Minus Fees): The provider then passes the remaining balance to you, minus their fees.

- You Invoice Your Customer: You send your customer an invoice with your agreed payment terms (e.g., 60 days).

- You Send a Copy to the Provider: You send a copy of that invoice to your finance provider.

- Customer Pays: Your customer eventually pays the full invoice amount.

The Two Main Types: Factoring vs. Discounting in 2026

When you look for invoice finance for retail businesses, you’ll mostly come across two terms: invoice factoring and invoice discounting.

- Invoice Factoring: This is where the invoice finance providers take over your credit control. They chase your customers for payment, and your customers are aware that you’re using a factoring service. For some retail businesses, especially smaller ones or those just starting with wholesale, this can be helpful as it frees up time and resources that would otherwise be spent on chasing payments.

- Invoice Discounting: It is often called “confidential invoice discounting.” Here, you retain control of your credit control. Your customers are usually unaware that you’re using a finance facility; they continue to pay you directly, and you then repay the finance provider. It is ideal for established retail businesses that want to maintain their direct customer relationships and have strong internal credit management.

Practical Benefits of Invoice Finance for UK Retailers

- Growth Without Debt: Unlike a traditional loan, invoice finance isn’t a debt in the conventional sense. It’s leveraging an asset (your invoices) that you already have. It keeps your balance sheet looking healthier and doesn’t tie up other assets as collateral.

- Always-On Cash Flow: No more waiting. You get instant access to funds, which means you can pay suppliers on time, take advantage of early payment discounts (saving you money!), and manage your operational costs smoothly.

- Seize Opportunities: Got a chance to buy a large batch of popular stock at a heavily discounted price? Invoice finance for retail businesses gives you the immediate cash to jump on such deals, giving you a competitive edge.

- Manage Seasonal Fluctuations: Stock up heavily before Christmas or the summer sale season without draining your bank account. You have the cash ready when you need it, and you repay it as sales come in.

- Outsource Credit Control (with Factoring): If chasing payments is a headache, factoring can offload that burden, letting you focus on sales, marketing, and product development.

How Best Invoice Finance UK Helps Retail Businesses

When choosing an invoice finance provider in the UK, you want someone who understands the specific pressures of the retail sector. Best Invoice Finance UK stands out for several reasons:

- Retail Sector Expertise: They understand the nuances of dealing with large retail chains, fashion houses, food distributors, and e-commerce platforms. It means they can tailor solutions that fit your specific payment cycles and customer base.

- Flexible Solutions: Whether you need full invoice factoring to handle collections or discreet invoice discounting services to maintain client relationships, they offer options that can be scaled up or down as your business needs change.

- High Advance Rates: They aim to provide high advance rates (often 90%+) on your invoices, ensuring you get the maximum amount of cash upfront.

- Quick Setup and Funding: For a retail business, time is money. They prioritise quick onboarding and ensure funds are in your account within 24-48 hours once an invoice is submitted.

Also Read:- Invoice Discounting Pros and Cons: Is It the Right Funding Option for Your Business?

Is Invoice Finance Right for Your Retail Business?

If your retail business primarily sells B2B (to other businesses rather than directly to consumers), has regular invoices, and faces long payment terms, then invoice finance for retail businesses is definitely worth exploring.

It’s a proactive way to manage your finances, smooth out your cash flow, and ensure you’re always ready to take advantage of the next big opportunity that comes your way. Don’t let cash flow bottlenecks slow down your retail empire. Unlock the capital tied up in your invoices and keep your shelves stocked and your business thriving.

FAQs

Q. Can I use invoice finance if I sell directly to consumers (B2C)?

Ans:- Generally no. Invoice finance providers require you to invoice other businesses (B2B) for the service to work, as they assess the creditworthiness of your business customer.

Q. What if my retail customer doesn’t pay?

Ans:- It depends on whether you have a “recourse” or “non-recourse” agreement. With “non-recourse,” the provider usually covers the loss from bad debt.

Q. Will my retail clients know I’m using invoice finance?

Ans:- With invoice discounting, no, it’s confidential. With invoice factoring, yes, they will be asked to pay the finance provider directly.

Q. Is it expensive compared to a bank loan?

Ans:- It can have a higher fee percentage, but it’s often more accessible, faster, and doesn’t require tangible collateral, making it a flexible alternative to traditional loans.

Q. How quickly can I get approved?

Ans:- Many UK finance providers can offer a decision within a few days, and once set up, funds for individual invoices can be advanced within 24-48 hours.

Discover the Latest Trends

Stay informed with our latest articles and resources.